The numbers tell one story about scale. The communities they serve tell another about significance.

Regularly, I find myself correcting misconceptions about what an independent theatre actually is.

Most people hear “independent theatre” and immediately think “indie cinema” — an arthouse venue

programming only specialty or non-mainstream films. While those theatres are certainly an important part of the independent landscape, that definition is far too narrow.

In reality, independent theatres are defined far more by ownership structure than by programming strategy.

Independent theatres are owned and operated by individuals, families, small private businesses, community nonprofit organizations, municipalities, colleges, and even public-school districts. What they are not is part of a major national or publicly traded circuit.

They may program arthouse films, studio blockbusters, repertory classics, faith-based content, concert films,alternative content — or a mix of everything. Their independence is rooted in who owns them and how they operate, not simply what happens to be on screen on Friday night.

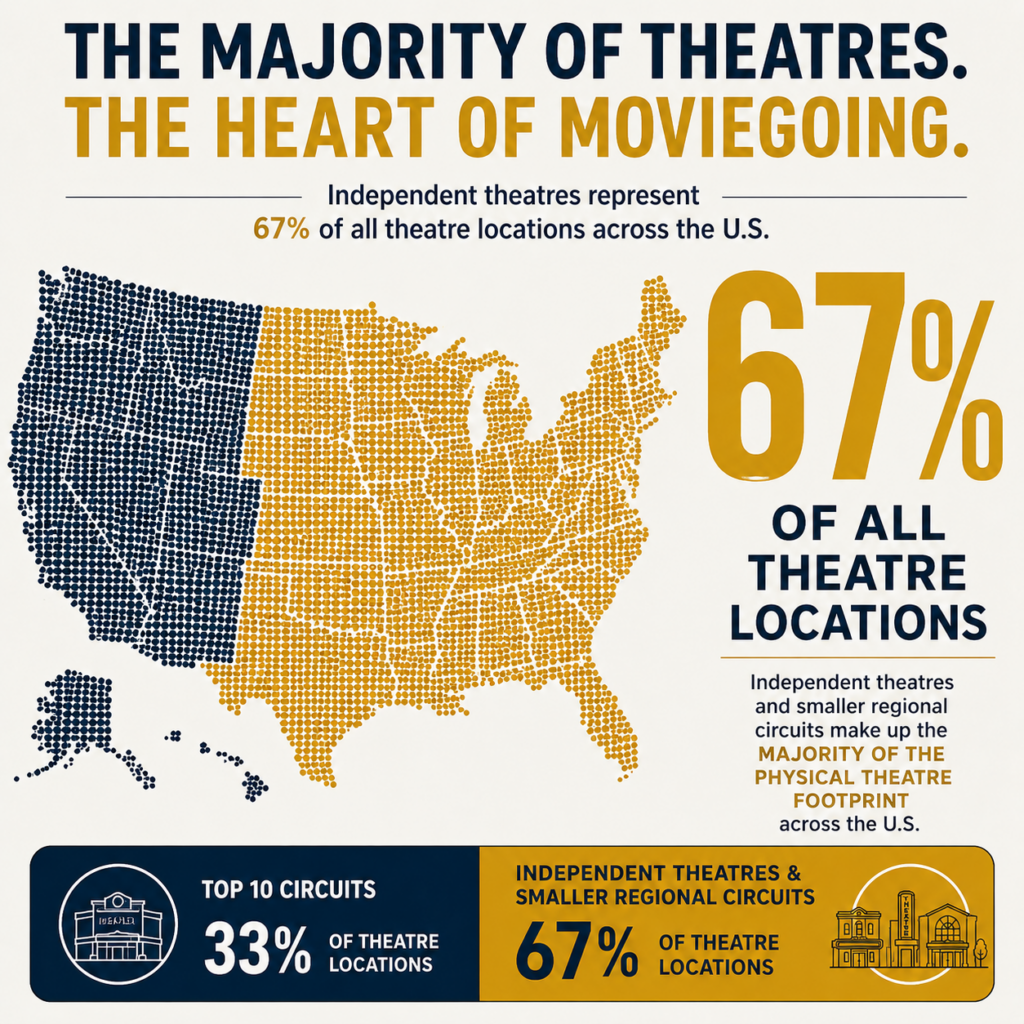

Structurally, the U.S./Canada exhibition market consists of approximately 36,500 screens across roughly 5,125 theatre locations. The top 10 circuits account for about 70% of the box office and 60% of all screens, while representing only one-third of theatre locations. On average, a top-10 circuit location operates roughly 13 screens — large-format multiplexes built for scale and concentration.

The remainder of the industry — largely independent operators and smaller regional circuits — accounts for 30% of the box office but spans 40% of all screens and an eye- popping 67% of all theatre locations. These venues average only about 4 screens per location, reflecting a fundamentally different model: smaller footprint, broader geographic reach, and far more points of physical presence across North

America.

Notably, approximately 25% of all theatre locations operate just one or two screens, underscoring just how much of the exhibition landscape is still built around small, community- based venues rather than large multiplex complexes.

Independent theatres are also disproportionately located in small and mid-sized markets. They often serve communities with smaller population bases and lower average ticket prices. As a result, average admissions revenue per screen can run roughly 60% lower than that of the top 10 circuits.

Yet despite their smaller footprint and thinner margins, independent theatres remain essential contributors to the broader box office ecosystem

And here’s the part that rarely shows up in the spreadsheets: independent theatres tend to mean a heck-of-a-lot more to their communities than a national chain megaplex means to its surrounding trade area.

These venues are often woven into the civic and cultural fabric of their towns. They’re downtown anchors, date-night traditions, fund-raiser hosts, school field-trip destinations, and the place where generations share a collective experience. When an independent theatre closes, it’s not just the loss of a retail outlet — it’s the loss of a gathering place, a heartbeat, a piece of local identity.

That distinction — scale versus significance — is what makes independent exhibition so important. They may be smaller in size, but in many communities, they are outsized in impact.